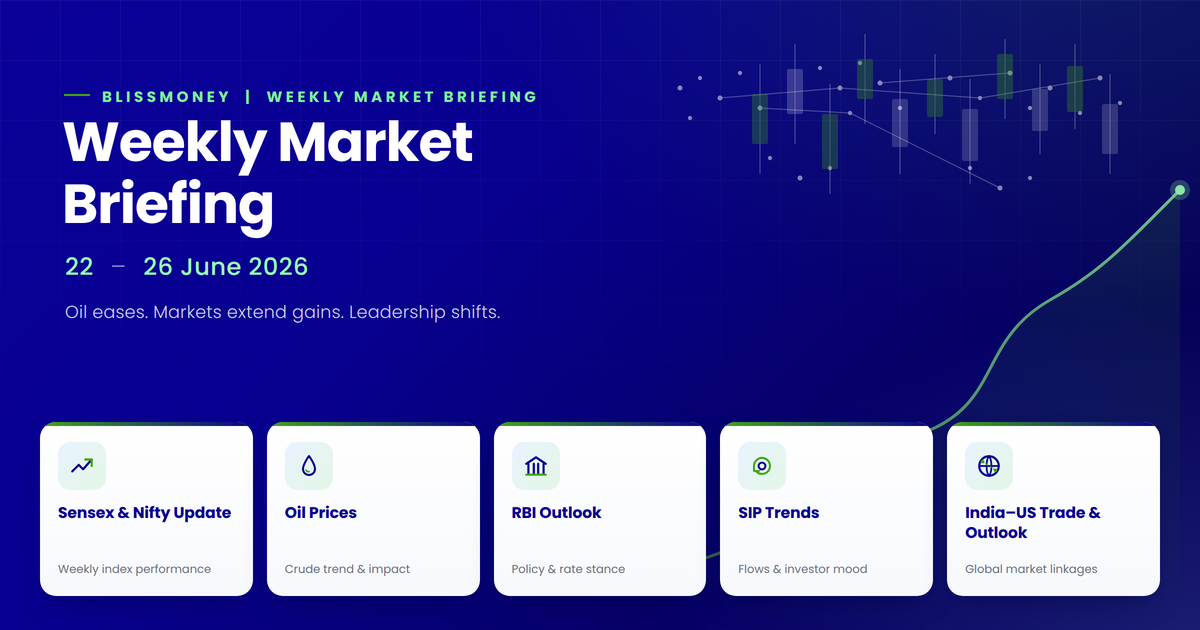

Weekly Indian Market Report: Sensex, Nifty, FII–DII Flows, Mutual Fund & SIP Trends

Blissmoney Weekly Market Report — Week Ending

1. Indian Markets — Sensex & Nifty Movement

Market Performance (Weekly Close):

Nifty 50 ended the week at ~25,966 points — a positive close after a volatile phase, recovering key levels.

BSE Sensex finished around ~84,978 points, up sharply on strong sectoral gains.

Market Drivers this Week:

- Global macro cues — softer US inflation data boosted optimism of future rate cuts, lifting Asian markets and supporting Indian equities.

- Sector breadth was broad, with banking, IT, and energy stocks contributing to the rally.

- Market volatility persisted, reflecting indecision and mixed sentiment among institutional investors.

Investor View:

Nifty’s reclaiming the ~25,900 level after a pullback signals short-term resilience, but the range-bound trading and technical indecision suggest caution for new positions until clearer trends emerge.

2. Institutional Activity — FII & DII

Here’s how Foreign Institutional Investors (FIIs) and Domestic Institutional Investors (DIIs) traded this week across the cash market (aggregated data to 19 Dec):

Weekly Net Activity (Cash Segment)

- FII Cash Activity: Net ~–₹251.9 crore, reflecting continued pressure on foreign portfolios

- DII Cash Activity: Net ~₹12,062 crore, showing strong domestic buying.

Interpretation:

- DIIs have been consistent net buyers, providing strong support to markets amid volatility.

- FIIs show mixed activity with intermittent buying and selling, but overall foreign cash flows remain cautious.

- Over the past 30 days, FIIs were net sellers while DIIs remained net buyers — highlighting domestic confidence in Indian equities.

Investor Takeaway:

Domestic institutions (mutual funds, insurance companies, banks) are acting as backbones of the market, while foreign money flows continue to be impacted by global macro uncertainty.

3. Mutual Funds — AUM, Inflows & SIP Trends

Mutual Fund Industry Snapshot (Nov 2025)

- Total Mutual Fund AUM: ~₹80.80 lakh crore — up steadily month-on-month and showing strong growth year-on-year.

- Net Equity Mutual Fund Inflows: ~₹29,894–₹29,911 crore in Nov 2025 — rising ~21% from October.

- SIP (Systematic Investment Plan) Trends

- Monthly SIP inflows (Nov 2025): ₹29,445 crore.

- Active SIP accounts: ~9.42–9.43 crore.

- SIP AUM (total SIP assets): ₹16.52 lakh crore — accounting for ~20.5% of total mutual fund AUM.

SIP flows remained near record high levels, even marginally lower than October, reflecting disciplined long-term investing.

Category & Strategy Movements

- Mid-cap and small-cap funds continue to attract allocations alongside large-cap strategies.

- Passive (ETFs) and hybrid funds also saw notable activity.

- Mutual funds also engaged in active secondary market trading — buying cores like BSE, Eicher Motors, HPCL as part of portfolio rebalancing.

Market Insight:

Retail investor participation through SIPs remains the foundation of MF flows, compensating for intermittent foreign outflows and adding stability to market liquidity.

4. Global Market Influence — Macro & Foreign Sentiment

Global cues such as US inflation data and potential Fed rate cuts supported risk assets, aiding Indian markets this week.

Despite this, 2025 saw continued foreign selling pressure with FIIs historically recording large net equity sales (~$18.4 billion) in India — indicating cautious global positioning.

This foreign sell pattern reinforces domestic accumulation as a critical stabilizer for Indian equities.

5. Wealth Management & Investor Strategy Insights

Investor Behaviour Trends

✔ Retail investors stick to long-term SIP strategies, a proven way to average cost and build disciplined portfolios — SIP AUM forming a significant part of total MF AUM.

✔ Strong domestic participation reduces volatility risk posed by foreign outflows.

✔ Hybrid & passive funds are gaining traction as investors balance growth with risk diversification.

Sector Notes for Investors

- Financials & Banking: Still a core driver of Nifty & Sensex gains this week.

- IT & Energy: Showed resilience on global cues and macro optimism.

- Mid & Small Caps: Continued interest from retail SIP and equitable flows.

Outlook — What Investors Should Watch Next Week

Market Triggers to Watch

- Upcoming macro data releases (GDP, inflation figures) — could steer domestic sentiment.

- Continued global central bank signals — especially US Fed policy expectations.

- FII flow direction — persistent foreign outflows vs. potential renewed inflows.

- Investment Views

- Long-term investors: Continue SIP allocations and diversified equity exposure.

- Short/medium-term traders: Monitor range support/resistance levels around Nifty ~25,900 and Sensex ~85,000.